Great question! In Colorado Springs, it’s not the norm to move in or take possession of the property prior to closing. It does happen but it’s not the norm.

Why is that?

There are a few primary reasons:

The transaction might not close. There’s a greater than zero chance a given transaction will not close. If the home sale were not to close and the seller has allowed a buyer to occupy a property, things can get messy.

The seller is at risk of increased liability. If something happens to or around the home, it’s likely the seller’s insurance policy which will have to cover it.

Home improvements can cause issues. If a seller allows a buyer to move in ahead of closing and the buyer starts making improvements and the property doesn’t close, who bears the cost of those improvements?

These are a few reasons it’s not likely and often not recommended for sellers to allow buyers to move in or occupy a property before closing.

If you are looking to buy or sell residential real estate in Colorado Springs, please give me – Rob Thompson, Realtor® – a call at 719-440-6626!

As a potential homebuyer, it’s essential to know what to look for during a home inspection to avoid costly surprises down the road. Here are the some things to look for during an inspection:

Roof – Check for any signs of damage or wear and tear, including missing shingles, leaks, or cracks.

Foundation – Look for any cracks or signs of settlement in the foundation, which could indicate structural issues.

Plumbing – Check all faucets, sinks, and toilets for leaks or damage, and ensure the water pressure is adequate.

Electrical – Make sure all outlets, light switches, and electrical panels are functioning properly and up to code.

HVAC – Inspect the heating and cooling systems to ensure they are in good working order and free of any leaks or damage.

Windows and doors – Check for any cracks or damage to windows and doors, and ensure they close and lock correctly.

Attic and insulation – Look for any signs of moisture or damage in the attic, and ensure the insulation is up to code.

Appliances – Test all appliances to ensure they are in good working order, including the stove, dishwasher, and refrigerator.

Exterior – Inspect the exterior of the home for any signs of damage, including cracks, rotting wood, or damage to the siding or stucco.

Safety features – Check for the presence and proper functioning of smoke detectors, carbon monoxide detectors, and other safety features.

Radon – test for levels of radon gas, which can be harmful if too high.

Sewer scope – inspect the main sewer line to check for any potential issues or blockages.

By taking the time to thoroughly inspect a home, you can ensure that you are making an informed decision and avoid any costly surprises down the road. This list is not all inclusive and is provided as a starting point.

If I can help with buying or selling a home, please let me know!

Rob Thompson, Realtor®, MBA, The Agency Colorado Springs 719-440-6626

Cash has the (significant) advantage of no appraisal but does it command the discount many feel it does? Let’s look at the data.

Below is a breakout of the purchase types of the sales YTD in the PPAR region. You can see there have been app 9,856 sales, 1646 of which have been cash. These on the average are paying 3.66% above list price. Contrast that with the 3.87% for conventional, 3.84% for FHA and 3.42% for VA and it’s immediately apparent that cash isn’t currently commanding the discount it has a reputation for.

Longer answer: the VA actually has no minimum credit score for insuring the loans of qualifying servicemembers. However, most lenders will require a minimum credit score.

There are lenders that offer loans to qualifying servicemembers with lower credit scores. There is always a cost, though. It’s usually in the form of a higher interest rate and higher loan costs.

That said, this can still be a good decision. There is something to be said about locking in housing costs vs renting, for example. But you have to run the numbers and do a cost benefit analysis.

I’m in a coding bootcamp but wanted to take a moment over lunch here to answer this question that I’m seeing pop up via email, PM and I’m also hearing more ads on the radio offering this.

I think this is a marketing tactic related to the rising interest rates and home prices (as companies try to generate additional revenue).

This is not legal or financial advice but I believe the short answer is: it depends.

The longer answer is it depends on your circumstances. While rolling high interest debt into your lower rate mortgage may sound good , there are a number of variables to consider, two of which are:

If you take the surplus of income and turn it around into paying down your home mortgage, that could be a good thing.

Doing so raises the value at which you have to sell your home (in a peaking market, this may cause trouble for you, if you have to sell).

What do I mean by the first option? If one has credit card debt of $25K that’s costing $450 in interest monthly, you may be able to roll that into a mortgage refi. But consider that may raise your mortgage payment. If it does so by $125, that leaves you $325. If you are disciplined and build an emergency fund with that or invest it or turn it back around into paying down the principal of the home, I could see this being a good option.

However!!! (emphasis intentional), know that it raises the amount you need to sell your home at by that corresponding value plus some (if you use a percentage based commission agent to sell, for example). If you are looking to stay in your home long term, that may still be a good option. But – and here’s the bottom line of this post – please understand it’s putting you in a position where you must have continued market appreciation to sell (unless you have a lot of equity).

And if you have a short horizon on home ownership, or are looking to sell soon, this could put you in a bad spot.

Let’s talk about S. 2155, “The Economic Growth, Regulatory Relief, and Consumer Protection Act” and the Veteran.

Buried deep (Section 309) in this bill (now law) are a couple of provisions that directly impact veterans with home loans (or veterans who will be getting home loans).

First, there’s a “Net Tangible Benefit Test” in which:

all of the fees and incurred costs are scheduled to be recouped on or before the date that is 36 months after the date of loan issuance

What does this mean?

Essentially, to refinance a VA loan, the total cost of the refinance must be less than or equal to the cost of the refinance over 36 months.

Is this a bad thing?

I submit that it is not. It protects the veteran from paying potentially extra dollars in fees. VA streamline refinances are often sold as “not having to pay anything up front to lower your payment!” This is true but there is a cost. That cost is added to the mortgage balance and reissued for 30 more years. This test imposes a test to make sure the veteran isn’t being taken advantage of in the form of higher fees.

Won’t this make it harder to refinance?

Potentially. However, it’s also going to put pressure on lenders to contain the VA refi costs.

The second provision address the minimum interest rate reduction:

in a case in which the original loan had a fixed rate mortgage interest rate and the refinanced loan will have a fixed rate mortgage interest rate, the refinanced loan has a mortgage interest rate that is not less than 50 basis points less than the previous loan

In short, these means the new loan will need to be approximately .5% lower than the previous loan. As with the test above, this doesn’t necessarily harm the veteran.

There’s long been a mantra in real estate – a rule of thumb – that suggests “It’s good to refinance if you can drop the rate 1% or more.” As a rule of thumb, this is good advice (but always run the numbers). It seems this provision codifies this rule of thumb into law in the form of “A veteran may not refinance unless the new interest rate is .5% or lower.”

Taken together, these provisions essentially state:

A veteran may not refinance unless the new interest rate is .5% or lower and the fees for the refinance are recoupable inside thirty-six months.

In sum, I submit these provisions are likely going to have the effect of protecting the veteran from being sold a product that is high cost for marginal gain.

There’s a common perception that, “Cash is King.” By this, it’s meant that cash tends to command a large discount.

Is that true in Colorado Springs?

Statistically not in December 2016.

There were 1,309 MLS listed sales for the month in the Pikes Peak Multiple Listing System (PPMLS) last month. Of those, 146 were cash. Of those 146, the average closing price to list price ratio was 98.3%.

Contrast that with VA loans for the same month, where the ratio was 100%.

Good question! This one came up several times over the last three days. The short answer is: Yes.

The longer answer is: Yes, but not all parties view earnest money the same way.

Earnest money is “skin in the game”. It’s money the buyer puts up after contract acceptance, to be held in escrow. This money is generally returned to the buyer at closing but MAY be forfeit to the seller, in certain circumstances. Earnest money is protected by several contractual protections for a buyer in Colorado.

This isn’t legal advice, just practical information. If you’d like to talk more about housing, please call Rob Thompson @ 719-440-6626!

Always consult a CPA for financial advice and an attorney for legal advice.

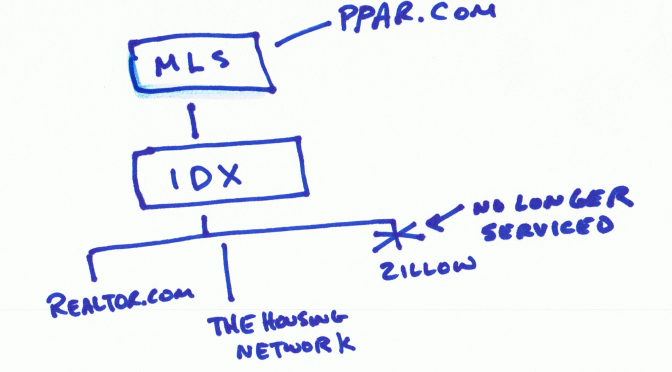

Good question! The short answer is: Yes, it is a tool you can use in your home search. But it has a limitation.

Zillow is a great platform for home searches and cannot/should not be discounted. However, there are a couple of things you should know when searching for homes in the Colorado Springs market.

Sites like this are fed from an IDX (Internet Data Exchange) via the MLS (Multiple Listing System).

awesome graphic from Rob

In the case of Zillow, it’s also manually updated by homeowners, property managers and agents. However, Zillow is no longer automatically updated by the local MLS. The result is that it no longer represents the totality of the market.

It is a tool in the search, but I also recommend checking TheHousingNetwork.com (full disclosure, that’s my website) and/or PPAR.com to see the current listings in the Pikes Peak region.

If you’re looking to buy or sell a home in Colorado Springs, I’d be honored to earn your business.

Short answer: yesno. Read the fine print.

Short answer: yesno. Read the fine print. I’m in a coding bootcamp but wanted to take a moment over lunch here to answer this question that I’m seeing pop up via email, PM and I’m also hearing more ads on the radio offering this.

I’m in a coding bootcamp but wanted to take a moment over lunch here to answer this question that I’m seeing pop up via email, PM and I’m also hearing more ads on the radio offering this.

There’s a common perception that, “Cash is King.” By this, it’s meant that cash tends to command a large discount.

There’s a common perception that, “Cash is King.” By this, it’s meant that cash tends to command a large discount.